SAN FRANCISCO—Sequoia global managing partner Doug Leone has accumulated a net worth of $3.8 billion over his three decades at the firm, according to the latest Forbes estimate. In the process, Leone has helped the VC juggernaut expand its investment scope well beyond its Menlo Park headquarters, with the firm opening additional offices in China, India, Israel and Singapore.

“We looked for places that we thought were going to grow rapidly and be very large,” Leone said Thursday at TechCrunch Disrupt. “We didn’t go to Europe because it was large but not growing. We didn’t go to Vietnam because it was growing but not large.”

Many VCs have shied away from investing in China because of its opaque financial regulations and strict government oversight that, among other things, requires companies to get licenses for IPOs, Leone explained, but Sequoia has done just the opposite. The firm now spends half its money in the region, and that trend isn’t likely to slow down anytime soon.

“It all depends on if you want to go where the puck is or where the puck is going to be,” Leone said. “It’s our belief that four or five years from now China is going to be a little different. There’s a lot of pressure now that China will become more open over time.”

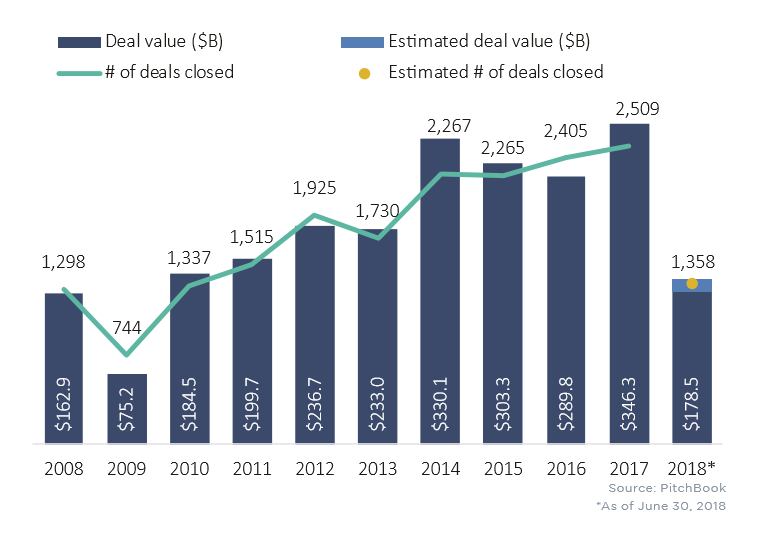

The country has already received increased attention in the VC industry over the past year, following the launch of SoftBank’s $100 billion Vision Fund. Sequoia has responded by targeting $8 billion for its latest investment vehicle, in what marks the largest US-based VC fund ever. The firm had reportedly raised $6 billion toward its massive target as of May, and Leone confirmed Thursday the fund has reached its $8 billion goal.

Why invest in China-based businesses, given the drawbacks? Leone argued that there are some advantages.

“Chinese founders in some ways are a little more desperate,” Leone said. “And you see it in the crazy work ethic that I’m not endorsing, nor condoning, nor disapproving. But I’ve had dinner in China at 10 pm. And people go to work after 10 pm. And we don’t see that in the US.”

Leone said Sequoia doesn’t directly compete with SoftBank and hasn’t lost out on any deals to the telecom giant. He disclosed that his firm has already made a pair of $400 million investments from its new $8 billion fund—totals that are more reminiscent of money spent by a private equity firm than a VC that specializes in growth investments.

“The reason we raised it is the large companies want to stay private longer,” Leone said. “They want to fight the global fight as private companies, not as public companies, and they require a lot more money in the private markets.

“Let me be clear, we have never lost a single company in this large fund to anybody because we have a preexisting relationship,” he added. “Having said that, we’re not going to get a discount price. We have to pay the market price.”